0

Under the advance tax system, income tax is required to be paid during the financial year in which the income is earned, rather than at the time of filing the Income Tax Return. This ensures a steady collection of taxes by the government and reduces the burden of lump-sum payment at year-end.

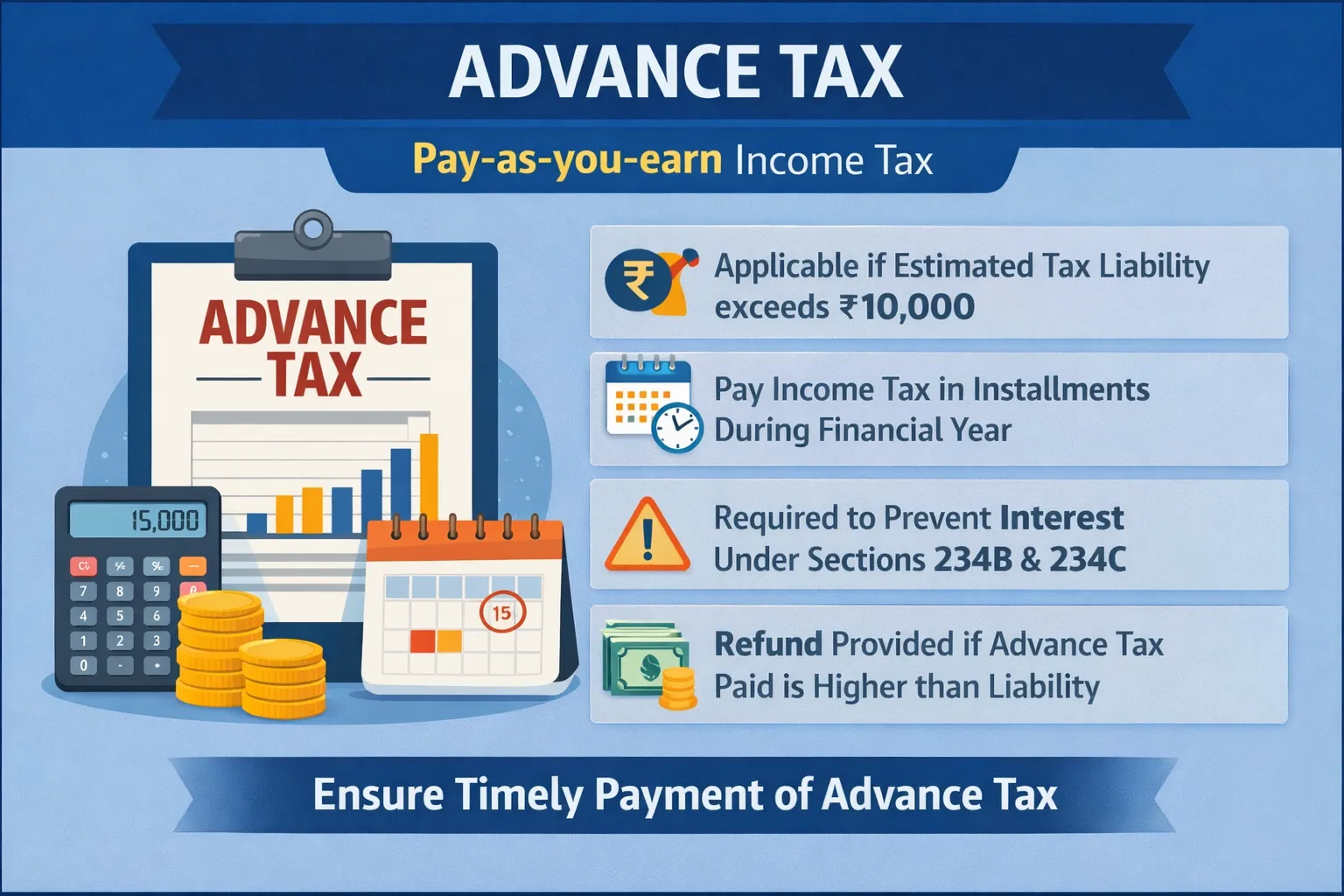

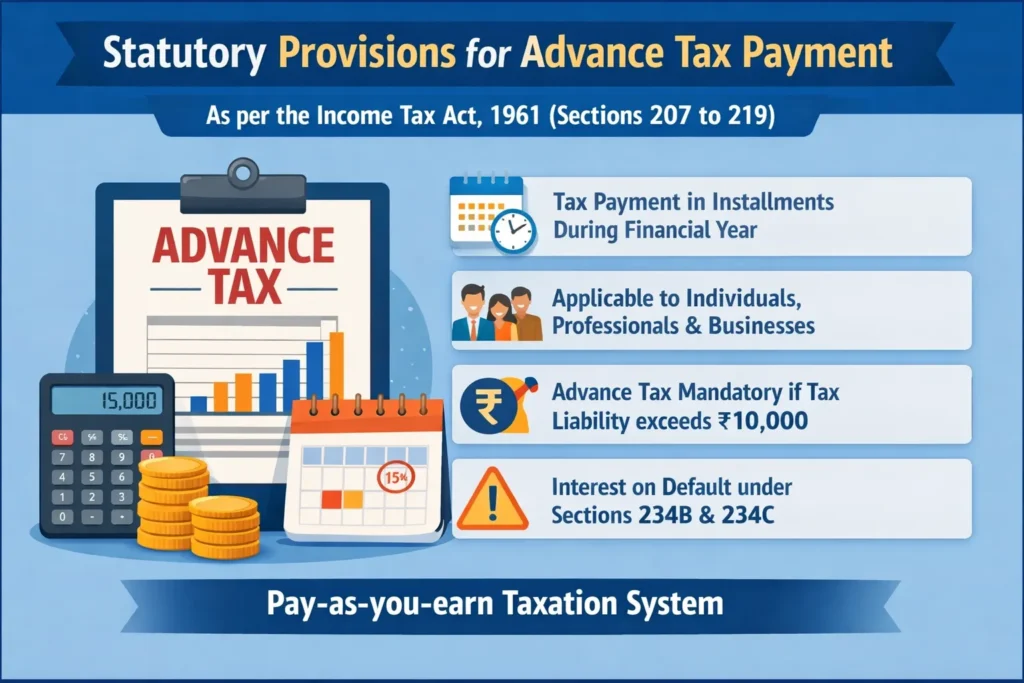

As per the Income Tax Act, a taxpayer is liable to pay advance tax if the total tax liability for the financial year exceeds ₹10,000.

Advance tax refers to the payment of income tax in installments during the financial year in which the income is earned, instead of paying the entire amount as a lump sum after the end of the financial year. It is commonly known as the “pay-as-you-earn” system of taxation.

The provisions relating to advance tax are contained in Sections 207 to 219 of the Income Tax Act, 1961.

Under this mechanism, a taxpayer estimates his or her total income for the financial year at the beginning (or during the course) of the year and accordingly computes the expected tax liability. Based on this estimated liability, advance tax is required to be paid in specified percentages across four installments, as per the due dates prescribed by the Income Tax Department.

As per Section 208 of the Income Tax Act, 1961, every assessee is required to pay advance tax if the estimated tax liability for the financial year exceeds ₹10,000.

The liability is determined after considering the total estimated income and calculating the expected tax payable for the year.

While computing advance tax liability:

The provisions of advance tax apply to:

In short, it applies to all categories of taxpayers, subject to the ₹10,000 threshold limit.

A special exemption is provided to certain senior citizens:

For regular taxpayers (individuals, professionals, businesses, and companies):

| Installment | Due Date | Minimum Advance Tax Payable |

|---|---|---|

| 1st Installment | 15th June 2025 | At least 15% of estimated tax liability |

| 2nd Installment | 15th September 2025 | At least 45% of liability (cumulative) |

| 3rd Installment | 15th December 2025 | At least 75% of liability (cumulative) |

| 4th Installment | 15th March 2026 | 100% of liability (cumulative) |

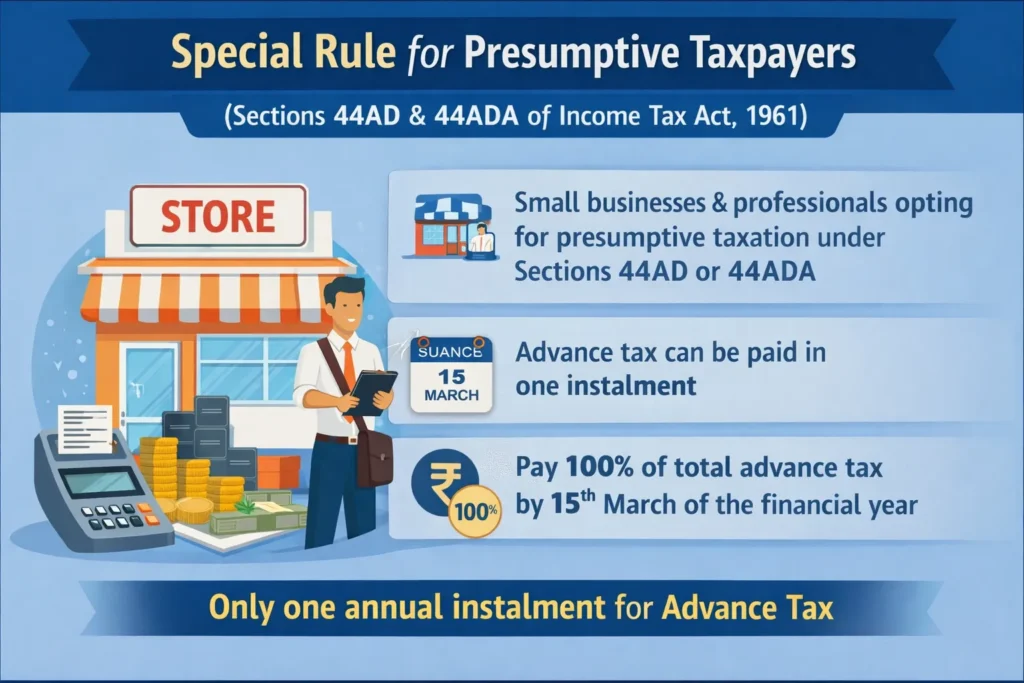

Taxpayers opting for presumptive taxation under Sections 44AD or 44ADA (small businesses/professionals) can pay their entire advance tax (100%) in one installment on or before 15th March 2026.

Advance tax can be paid easily through the Income Tax e-Filing Portal. Below is a step-by-step professional guide:

Go to: https://www.incometax.gov.in

You can pay advance tax:

On the homepage:

Enter:

Choose:

Fill in:

The system will auto-calculate the total payable amount.

You can pay via:

After successful payment:

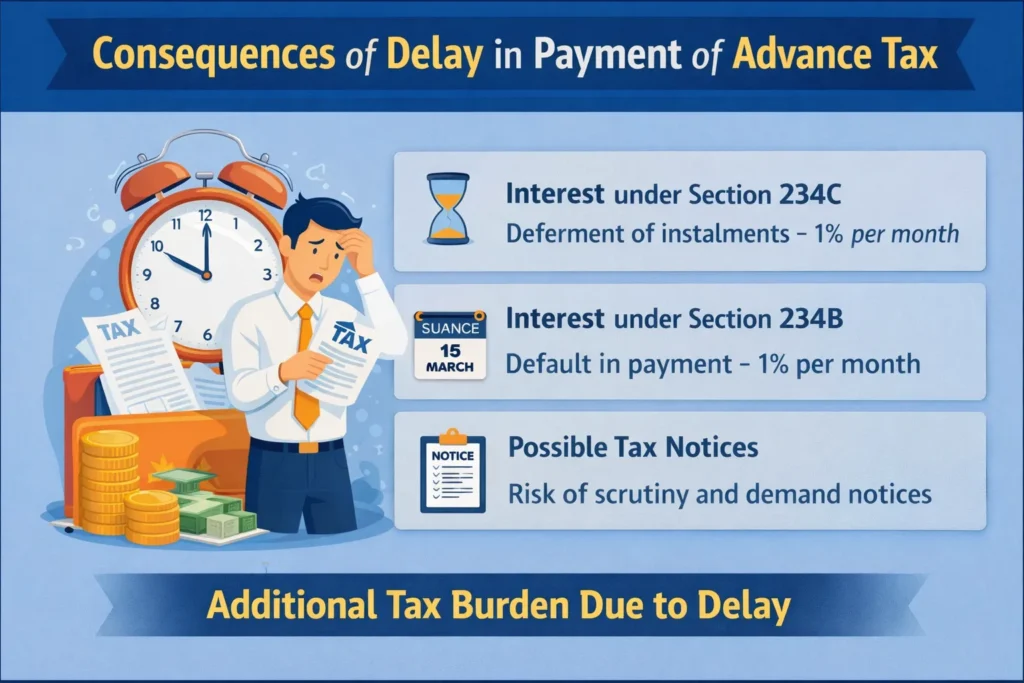

Timely payment of advance tax is a statutory obligation. Delay or short payment may lead to financial implications in the form of interest and possible notices from the Income Tax Department.

If a taxpayer fails to pay the required percentage of advance tax by the prescribed due dates, interest under Section 234C is applicable.

If:

Then interest under Section 234B will apply.

Delay results in:

## Even if TDS is deducted, taxpayers must ensure that the remaining tax liability (if any) is discharged through advance tax to avoid interest liability.

It is essential for taxpayers to pay advance tax within the prescribed due dates whenever applicable. Non-payment or short payment of advance tax may attract interest under Section 234B (for default in payment of advance tax) and Section 234C (for deferment of advance tax installments) of the Income Tax Act, 1961. Interest under both sections is generally levied at 1% per month or part of a month, as applicable.

On the other hand, if a taxpayer has paid excess advance tax compared to the actual tax liability, the excess amount is eligible for refund, subject to adjustment at the time of filing the Income Tax Return. The refund, if any, will be processed by the Income Tax Department along with applicable interest under Section 244A, where eligible.

Advance tax is income tax paid in installments during the financial year instead of paying the entire amount at the time of filing the Income Tax Return.

Any taxpayer whose estimated tax liability for the financial year is ₹10,000 or more after adjusting TDS/TCS is required to pay advance tax.

Yes, if TDS deducted by the employer is insufficient and the remaining tax liability exceeds ₹10,000, salaried individuals must pay advance tax.

Senior citizens (aged 60 years or more) not having income from business or profession are exempt from paying advance tax.

However, those having business or professional income must comply.

For regular taxpayers, advance tax is payable in four installments:

Taxpayers opting for presumptive taxation under Sections 44AD or 44ADA can pay the entire advance tax in one installment on or before 15 March of the financial year.

Interest may be charged under:

Interest is generally levied at 1% per month or part thereof.

Yes, if advance tax paid exceeds actual tax liability, the excess amount will be refunded after filing the Income Tax Return, along with applicable interest under Section 244A.

Advance tax can be paid online through the Income Tax e-Filing Portal using Challan 280 (Advance Tax—Code 100).

Yes, freelancers, consultants, and professionals must pay advance tax if their estimated tax liability exceeds ₹10,000.