0

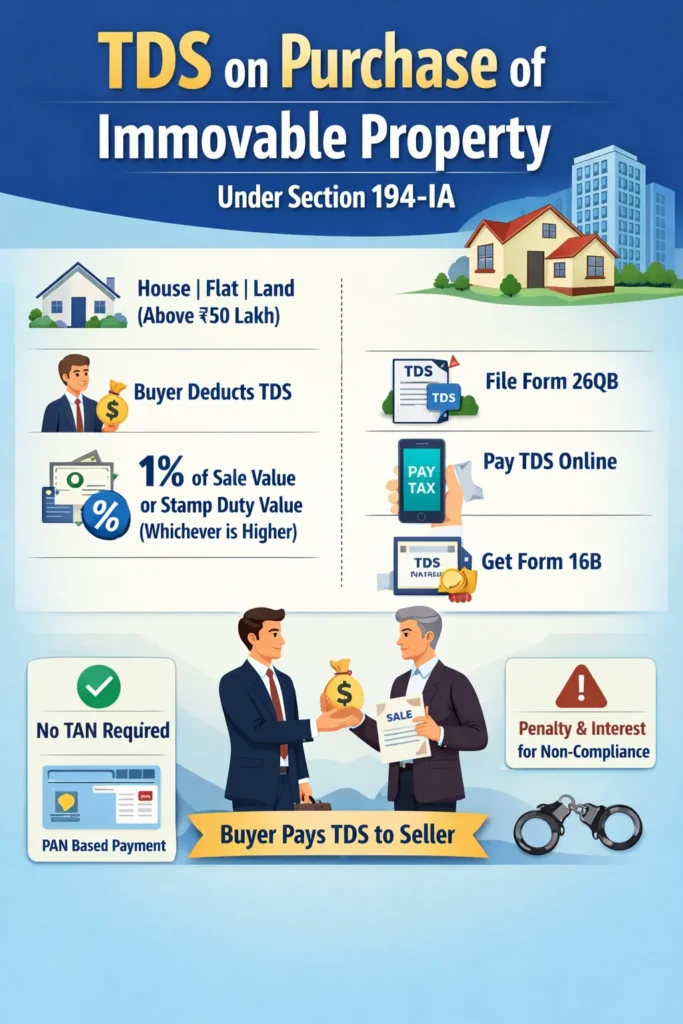

Under Section 194-IA of the Income-tax Act, 1961, any person (buyer) responsible for paying consideration for the transfer of an immovable property—such as a house, apartment, building, or land (other than agricultural land)—is required to deduct Tax Deducted at Source (TDS) at the time of payment to the seller.

The buyer must deduct TDS at the rate of 1% on the higher of:

This provision applies where the transaction value meets the prescribed threshold under the Act.

As per the amendments introduced in the Union Budget 2026, a significant compliance relief has been provided:

This amendment simplifies the compliance process and reduces procedural burden for buyers involved in such transactions.

Section 194-IA of the Income-tax Act, 1961 deals with Tax Deducted at Source (TDS) on the purchase of immovable property.

It requires the buyer of immovable property (other than agricultural land) to deduct TDS while making payment to the seller.

(TDS on Purchase of Immovable Property)

Section 194-IA of the Income-tax Act, 1961 lays down specific conditions that must be fulfilled for TDS to be applicable on the purchase of immovable property.

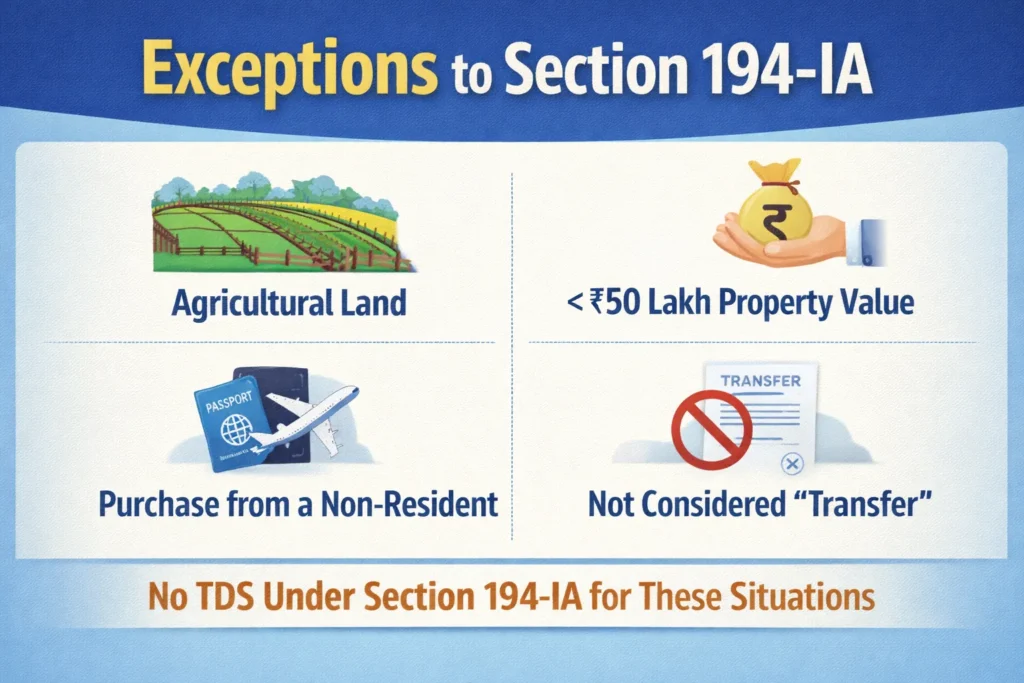

While Section 194-IA of the Income-tax Act, 1961 mandates TDS on the purchase of immovable property, the following situations are not covered under this section:

No TDS is required if the property transferred is agricultural land (not being land situated in specified urban areas as per the Income-tax Act).

If the sale consideration is less than ₹50 lakh, Section 194-IA does not apply.

However, if the consideration is ₹50 lakh or more, TDS becomes applicable.

If the seller is a non-resident, Section 194-IA does not apply.

Instead, TDS provisions of Section 195 of the Income-tax Act, 1961 will apply, and TDS must be deducted at the rates applicable to non-residents.

If the transaction does not amount to a transfer under the Income-tax Act (for example, certain inheritance or gift transactions), TDS under Section 194-IA may not apply.

In certain cases of compulsory acquisition, separate TDS provisions may apply instead of Section 194-IA.

Even if the buyer is an individual or not engaged in business, Section 194-IA still applies if the conditions are met. There is no exemption based on turnover or audit requirement.

(As per Section 194-IA of the Income-tax Act, 1961)

When purchasing immovable property (other than agricultural land) for ₹50 lakh or more, the buyer must deduct 1% TDS and deposit it using Form 26QB. After payment, Form 16B (TDS Certificate) must be issued to the seller.

Below is the complete step-by-step process:

When purchasing immovable property (other than agricultural land) for ₹50 lakh or more, the buyer must deduct 1% TDS and deposit it using Form 26QB. After payment, Form 16B (TDS Certificate) must be issued to the seller.

Below is the complete step-by-step process:

Go to the official website https://www.incometax.gov.in of the Income Tax Department

Ensure PAN details are correct to avoid Form 16B issues.

Provide the following information:

Choose one of the following:

Due Date: Within 30 days from the end of the month in which TDS was deducted.

Form 16B must be issued to the seller within 15 days from the due date of filing Form 26QB.

Visit TDS Reconciliation Analysis and Correction Enabling System (TRACES) https://www.tdscpc.gov.in

Register as a taxpayer using PAN (if not already registered).

Submit the request.

Failure to comply with Section 194-IA of the Income-tax Act, 1961 can lead to interest, penalty, and other legal consequences for the buyer (who is responsible for deducting and depositing TDS).

If TDS is not deducted:

If TDS is deducted but not deposited:

If Form 26QB is not filed within the due date:

The Assessing Officer may levy penalty:

In certain cases involving business transactions, non-compliance may attract disallowance under Section 40(a)(ia).

In extreme cases of willful default, prosecution provisions may apply under the Income-tax Act.

It is a provision that requires the buyer of immovable property (other than agricultural land) to deduct 1% TDS when the sale consideration is ₹50 lakh or more.

TDS is deducted at 1% on the higher of:

No. If the sale consideration is less than ₹50 lakh, TDS under Section 194-IA is not applicable.

No. The buyer is not required to obtain TAN. TDS can be paid using PAN through Form 26QB on the Income Tax Portal of the Income Tax Department.

TDS must be deposited within 30 days from the end of the month in which deduction is made.

Form 26QB is a challan-cum-statement used for payment of TDS on property purchase.

Form 16B is the TDS certificate that the buyer must issue to the seller after depositing TDS. It can be downloaded from the TDS Reconciliation Analysis and Correction Enabling System (TRACES) portal.

Yes. If payment is made in installments, TDS must be deducted on each installment.

Separate Form 26QB must be filed for each buyer–seller combination.

The buyer may have to pay:

No. In such cases, Section 195 of the Income-tax Act, 1961 applies instead.