0

When an individual sends money abroad, the transaction may attract Tax Collected at Source (TCS), commonly referred to as foreign remittance tax in India.

As per Section 206C(1G) of the Income Tax Act, 1961, banks and other Authorized Dealers (ADs) are required to collect TCS at the prescribed rates at the time of transferring funds overseas under the Liberalized Remittance Scheme (LRS).

The TCS collected is not an additional tax but is reflected in the taxpayer’s Form 26AS and can be claimed as a credit or refund while filing the Income Tax Return, subject to eligibility.

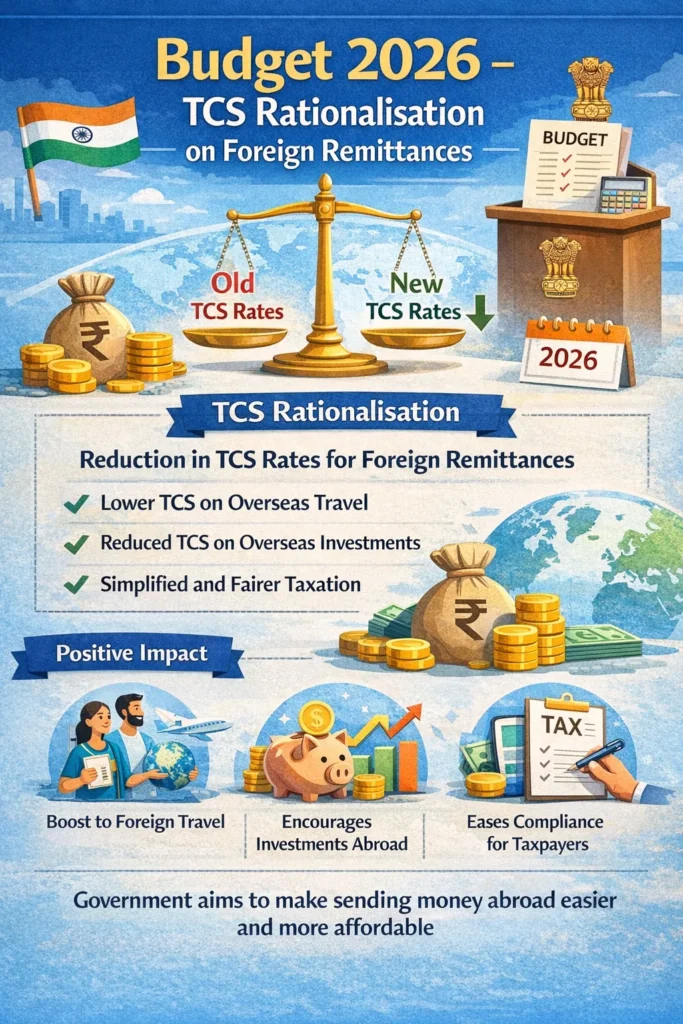

In the Union Budget 2026–27, the Government of India has proposed significant reductions in the Tax Collected at Source (TCS) applicable to certain overseas remittances under the Liberalised Remittance Scheme (LRS):

• Education and Medical Remittances: The TCS rate on remittances for education and medical purposes under the LRS has been reduced from 5% to 2%. This reduction is intended to ease the upfront cash outflow for individuals transferring funds abroad for these essential purposes.

• Overseas Tour Programme Packages: The TCS on overseas tour packages has been simplified to a flat 2% with no monetary threshold. Previously, the rate varied (5% up to ₹10 lakh and 20% above ₹10 lakh), but the budget proposes a uniform 2% rate regardless of the package value.

These changes are part of a broader rationalization of TCS provisions and are proposed to take effect from 1 April 2026 upon enactment of the Finance Bill.

Tax Collected at Source (TCS) on foreign remittance applies when an Indian resident transfers money outside India under the Reserve Bank of India’s Liberalised Remittance Scheme (LRS).

Under this provision, the authorized dealer or bank collects TCS at a prescribed percentage on the amount remitted and deposits it with the Government of India on behalf of the remitter.

Certain foreign remittances are exempt from Tax Collected at Source (TCS) under the Liberalised Remittance Scheme (LRS). These exemptions help reduce the tax burden in specific situations.

The following remittances are not subject to TCS:

Note:

These exemptions apply only to eligible outward remittances made by Indian residents under the LRS. Any remittance not covered under the above categories may still attract TCS at the applicable rates.

Riya takes an education loan from a bank to study in the UK.

Her bank remits ₹15 lakh directly to the foreign university.

Amit sends ₹8 lakh from his savings to pay his daughter’s college fees in Australia.

Neha remits ₹6 lakh to a hospital in Germany for her father’s medical treatment.

Rahul travels to Europe and spends ₹3 lakh using his international credit card on hotels, food, and shopping.

## TCS on foreign remittance does not apply in genuine education and medical cases (within limits) and on bank-funded education loans. Even where TCS is collected, it is adjustable or refundable while filing your income tax return.

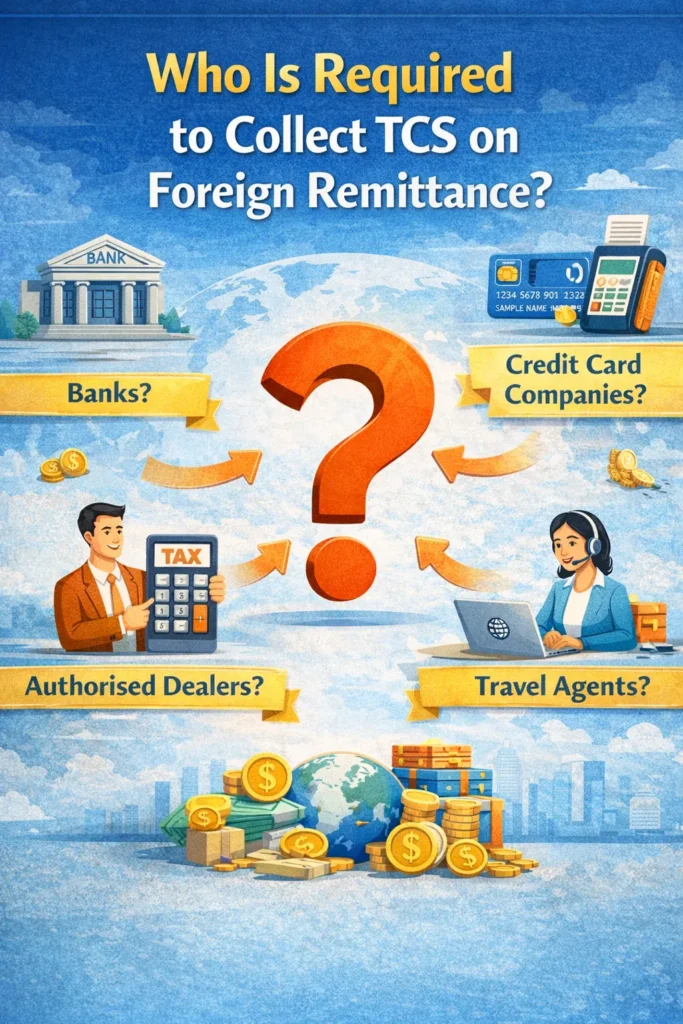

Under Section 206C(1G) of the Income Tax Act, 1961, the responsibility to collect Tax Collected at Source (TCS) on foreign remittances lies with the Authorised Dealer (AD) facilitating the transaction.

Specifically, TCS must be collected by:

If you are sending money abroad, your bank or authorized forex dealer will automatically collect the applicable TCS and deposit it with the government on your behalf.

When you send money abroad under the Liberalised Remittance Scheme (LRS), banks or authorised dealers may collect Tax Collected at Source (TCS) on the transaction. This TCS is not a final tax but a credit available to the remitter. To ensure you receive the benefit of the TCS collected, it is important to verify that the amount has been correctly reported and to claim it while filing your Income Tax Return. The following steps explain how you can easily check and claim TCS on foreign remittances.

After remitting money abroad, the bank or authorized dealer collects TCS and deposits it with the government.

You can verify this TCS credit by:

The TCS amount collected on your foreign remittance will be reflected here.

You can also cross-check the TCS details in your Annual Information Statement (AIS) available on the income tax portal.

This helps ensure that the remittance and TCS details reported by the bank are accurate.

While filing your Income Tax Return (ITR):

Indian residents can transfer money to the USA under the RBI’s Liberalised Remittance Scheme (LRS), subject to prescribed limits and compliance requirements.

You can send money to the USA using any of the following methods:

You will need to submit the following:

Failure to comply with the provisions relating to Tax Collected at Source (TCS) on foreign remittances can lead to financial and legal consequences, particularly for banks and authorized dealers, and in some cases for the remitter.

TCS (Tax Collected at Source) on foreign remittance is a tax collected by banks or authorised dealers when an Indian resident sends money abroad under the Liberalised Remittance Scheme (LRS), as per Section 206C(1G) of the Income Tax Act.

TCS is collected by the authorised dealer, such as:

The remitter does not pay TCS directly to the government.

No. TCS is not an additional tax. It is only a tax credit that can be:

You can check the TCS amount in:

No. TCS applies only to outward foreign remittances under LRS.

Inward remittances (money received from abroad) are not subject to TCS.

Yes. TCS is not applicable in the following cases:

If PAN is not furnished:

Providing PAN is mandatory for smooth processing.

TCS is collected by the authorised dealer:

Yes. If your final tax liability is lower than the TCS collected, or if you have no tax liability, you can claim a refund while filing your ITR.

No. TCS does not reduce the annual LRS limit of USD 250,000. It is calculated over and above the remitted amount.

Non-compliance can lead to: